From “Feeding 9 billion” to “Overproducing”

The current agriculture vibe shift

In 2009, the Food and Agriculture Organization of the United Nations made a dire prediction: by 2050, there would be over 9 billion people on earth and farmers across the globe would need to grow 70% more food to support the growing population.

Standing here in 2026, where caring is apparently “cringe,” it’s difficult to describe the way in which “feed 9 billion” became an earnest call to arms for so many across the industry. In the show Silicon Valley, there is a punchline that every tech company in the early 2000s just wanted to “make the world a better place.” The agriculture industry’s version of this was that every company just wanted to help “feed the world.”

While Janette Barnard has beaten me to the punch by several years in explaining why “feed the world” is sooo 2009, this industry rallying cry did motivate the agriculture industry to focus relentlessly and singularly on increasing yield.

Lately, I’ve noticed a vibe shift, particularly in the US commodity crop corner. No longer is it “feed the world” or “feed 9 billion.” There’s a new message I’ve been hearing more and more, a steady drumbeat getting louder:

“We are overproducing.”

To be fair, environmentalists have been saying this for a while. However, more and varied voices are joining the chorus, with diverse reasons beyond environmental concerns:

Often, “overproduction” is used as a set-up to a favored solution: stop farming poor ground, chug more biofuels, decommodify commodities, break up monopolies, diversify crop mix, make “food is medicine” instead of “food is food/fuel/fiber,” or insert-your-agriculture-agenda-here.

Before we declare the culprit as “overproduction” and that becomes the marching order for the next fifteen years, I want to know if it’s true. And if “overproduction” is the villain, what does that actually mean?

Let’s dig in!

Reality check: what does the data say

You don’t hear people saying “we grow too much spinach!”

Instead, the “overproduction” label is applied squarely to commodity crops like corn and soybeans. This makes sense as corn and soybeans are grown on a majority of the farmed acres in the US and world, and when harvested are exported globally and used for biofuels and livestock feed. We’ll focus on this argument today.

So how much corn and soybeans are actually produced in the US? And how does that compare to how much is left over in any given year?

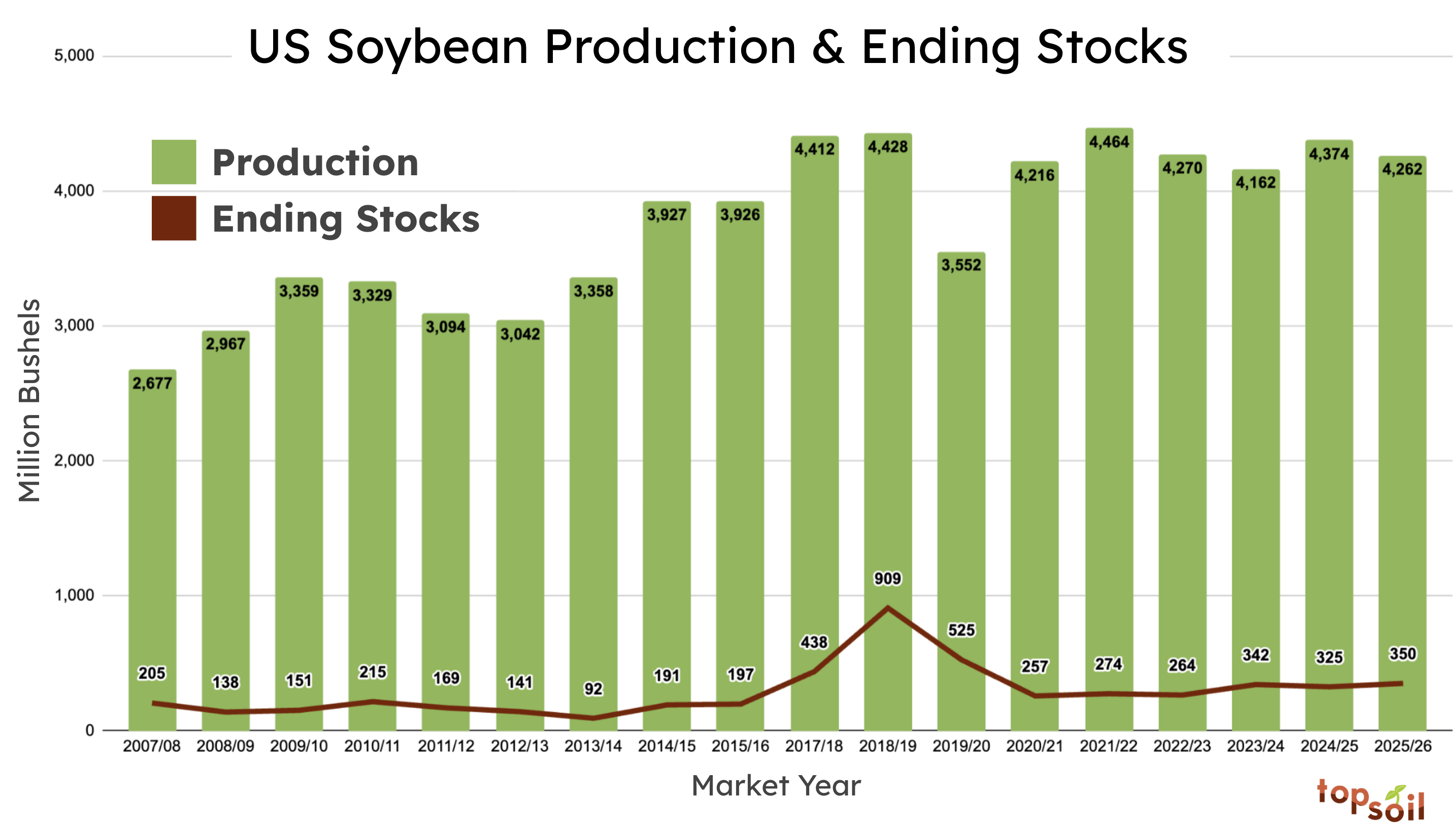

When we look at soybean production in the US over the past nearly two decades, the trend is up and to the right. American farmers grow nearly 60% more soybeans today than in 2007. Now that’s what I call yieldsmaxxing!

At the same time, the “Ending Stocks,” or how much is left over in storage from one year to the next, has remained steady as a share of production, around 8%. This means that even though production has increased dramatically, somehow, over 90% of soybeans have found a job and demand has kept up.

You’ll notice one discrepancy in this chart. In 2018, with the first blows of the US-China trade war, the ending stocks ballooned up to 20% of the total production that year. Farmers reacted in 2019 by growing much less soybeans. In the most recent rounds of the trade war, ending stocks have not spiked and have remained steady instead.

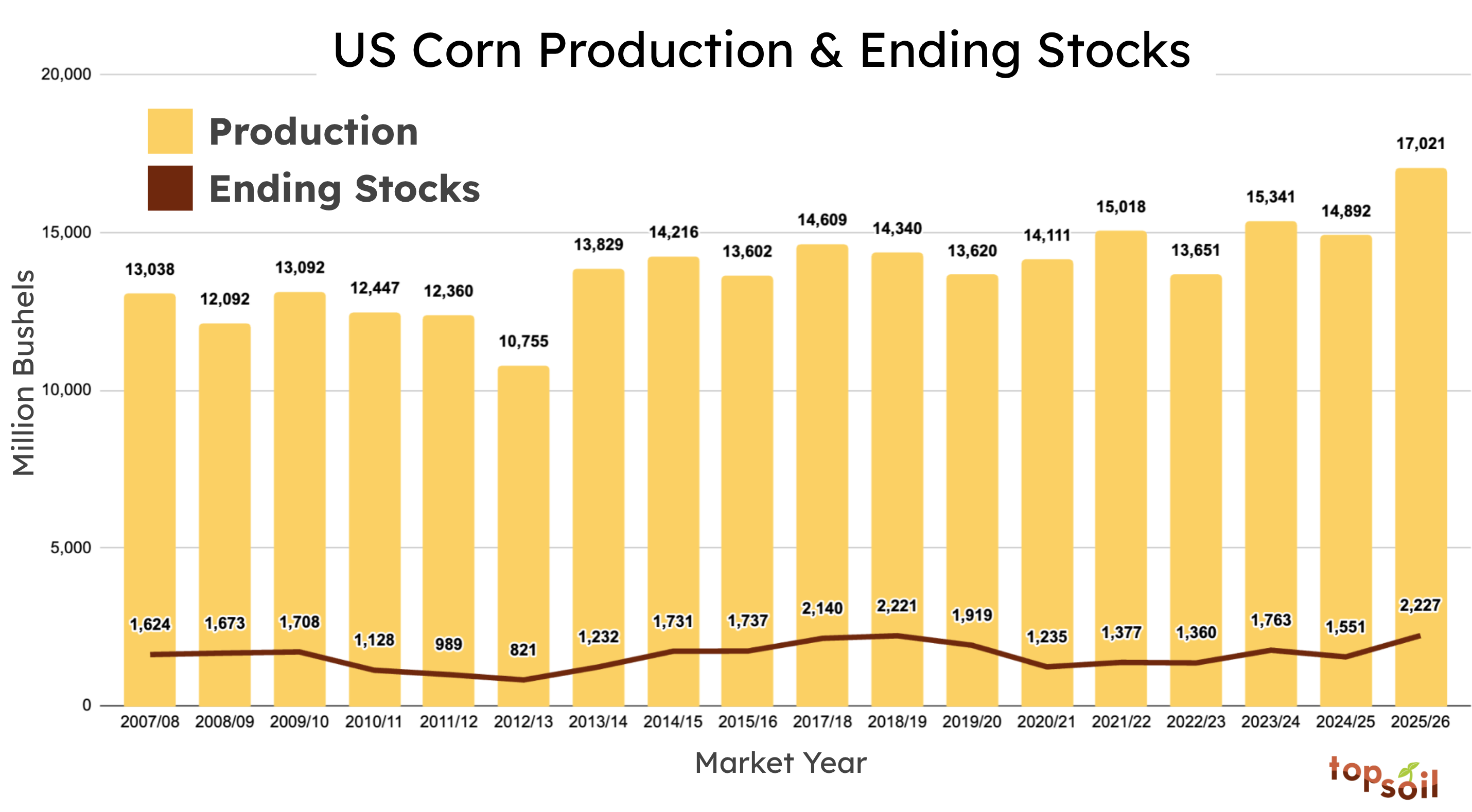

Corn production over the past two decades has increased by 30%. While this 30% is about half of the relative growth that soybeans experienced, keep in mind that the corn crop is much larger than the soybean crop (the average acre of corn produces ~200 bushels and the average acre of soybeans ~60 bushels). The increase in corn production over the time period represents nearly 4 billion more bushels (about the size of the entire 2025 soybean crop).

Despite the increase in corn production, the amount left over in any given year has remained steady around 11% of production. In 2025, the ending stocks ticked up to 13%. Given 2025 featured a monster crop over 2 billion bushels bigger than 2024, that is expected.

Looking at this data, we’ve established that American farmers are certainly growing more corn and soybeans than ever before. However, this new supply is getting absorbed, as the ending stocks haven’t been rising along with production.

No doubt we are producing, but what might we actually mean when we say “overproducing”?

Creative way to call out low prices

When corn was flying high at $8 per bushel back in 2012, of course farmers wished they were growing more. But no one was shaking their fist on LinkedIn that the entire agricultural sector was “underproducing!”

When people decry “overproduction” today, it’s likely they are really just saying “prices are too low.” Specifically, that prices are too damn low for farmers to turn a profit.

This is the likeliest culprit – especially when we look at farmers’ bottom lines. In 2025 in the US, farmers were losing an average of $50 to $60 per acre of corn or soybeans.

In a market-driven commodity market, when more is produced than demanded, prices drop until a new steady state price is reached. Today, that price is 40% below the all-time high for soybeans and almost 50% lower than the all-time high for corn.

Meanwhile, prices for the inputs to produce a crop, like fertilizer, fuel, labor, interest, and crop protection have remained stubbornly high, squeezing the farmer.

Even though demand has kept up with the increasing supply enough to soak up all of the billions of additional bushels grown in the past 20 years, this new demand has not translated into farmer profitability.

Is it really about where the supply is coming from?

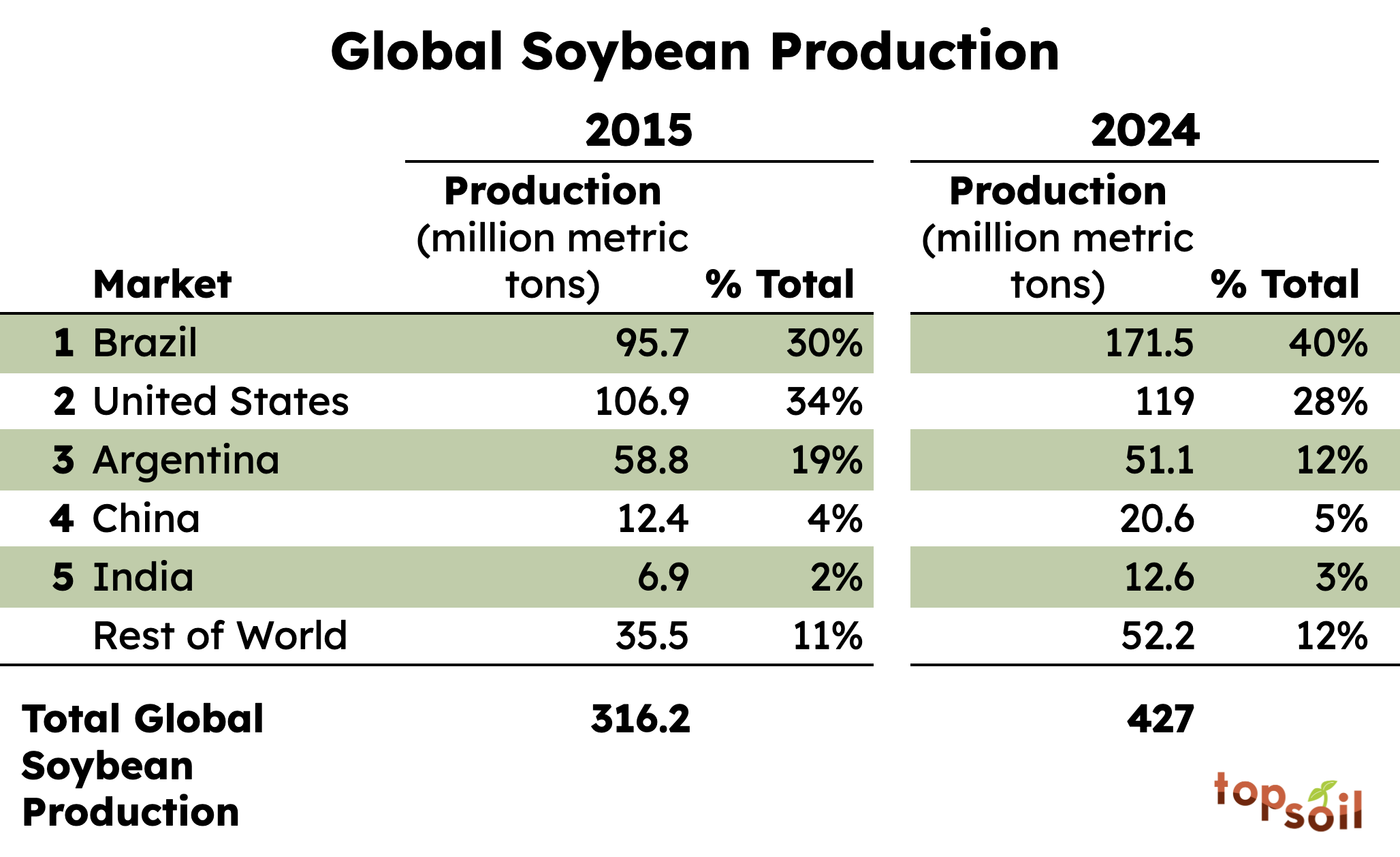

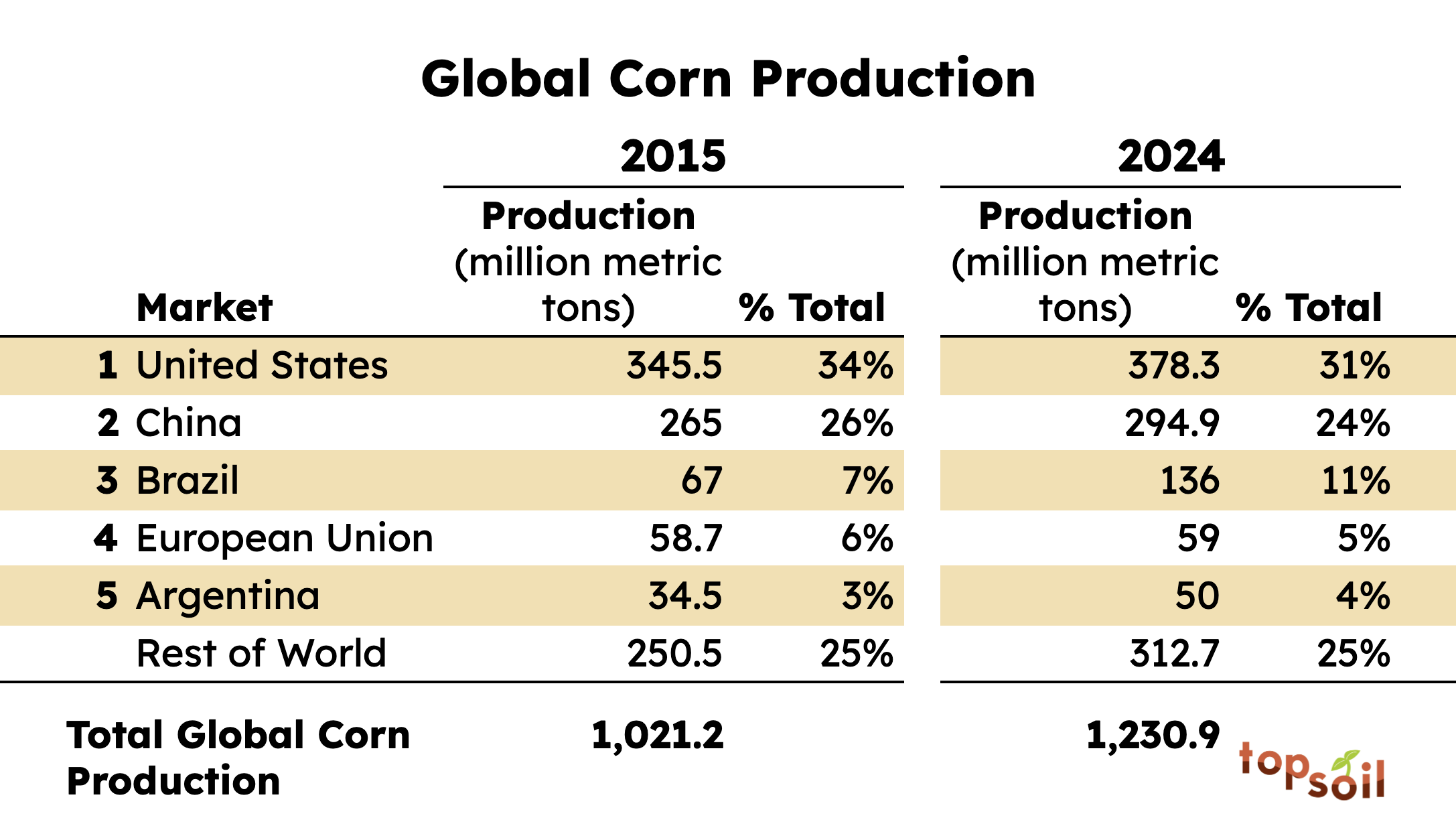

My media diet is heavily attuned to US Midwestern row crop farmers. However, the biggest story in corn, and especially soybeans, in the last decade is Brazil.

Today, Brazil is the undisputed leader in soybean production, growing 40% of the world’s soybeans. That was not the case a decade ago, when the US was in pole position.

In the past 10 years, Brazil has also more than doubled corn production. While Brazil is still a distant third to the US and China, it’s important to note that very little of China’s corn is exported, which again leaves the US and Brazil competing to fulfill global export demand.

In the not-so-distant past, a huge portion of exported corn and soybeans were produced in the Northern Hemisphere. This meant that every autumn, there was one big harvest that would get exported around the globe. Prices would drop as the market flooded with new grain in the fall. As the year wore on, prices crept up as stored grain dwindled, before the next harvest provided certainty around how much grain would be available for the coming year.

These price fluctuations meant that farmers who could store their grain could take advantage when prices would spike.

Brazil, as you may be well aware, is in the Southern Hemisphere. Brazilian grain is harvested around March and April for soybeans, and from February to August for the two corn crops per year. Instead of one big motherload of grain hitting the global market once per year, now grain enters the market several times per year.

Grain buyers suddenly have more options, and more certainty, meaning that the “summer price rally” is no longer a profit-taking opportunity for farmers. It costs more to produce grain in the US than in Brazil, so the North American farmer feels this squeeze more, too.

Is it really about demand?

Corn and soybeans are commodities. By definition, soybeans grown in Missouri are interchangeable with soybeans grown in Mato Grosso (I know some of you will say that the grain composition might differ or there might be regional quality differences, but bear with me here). At any given moment, there is one global price for corn or soybeans.

The physical reality is quite different. A single harvested bushel of corn is a 56-pound collection of ~80,000 tiny little pieces that have to be carefully protected from moisture and stored with specialized equipment. Now, imagine the 17 billion bushels of corn produced in the US in 2025 alone – heavy, bulky, and generally a pain in the ass to move around. As a result, the price that a farmer is able to sell their grain is based on where they can sell their grain.

Where a farmer can sell their grain is highly dependent on who nearby can export or make use of that grain. There has been diligent investment to create demand for the billions of bushels grown every year, from biofuels, to more livestock to feed, to new materials, to new export markets. This demand isn’t unlimited, however.

As trade disputes have cleaved the world anew, farmers’ access to export markets has changed. And while market access has shifted, the existing infrastructure and sheer physics of moving grain has not.

Notably, China previously bought about a quarter of US soybeans. As trade tensions worsened through the fall of 2025, purchases from the US screeched to a halt. Since November, China purchased 12 million tons of US soybeans (about half of what was purchased in 2023) in line with a US-China trade agreement. Since that commitment was met, China has returned to importing soybeans from South America that are ~$0.50/bushel (about 5%) cheaper than US soybeans.

Creating new markets to replace the previous demand by China requires building relationships and infrastructure, both of which can take years, if not decades, of effort. Growing more livestock, creating more demand for biofuels, or inventing new materials takes time as well, and there are no guarantees that new demand will magically materialize.

Beyond “overproducing”

It’s high time that we move beyond the simple rallying cry of “feed 9 billion.” And yet, “we’re overproducing” is an over-simplification, too.

Just as there is no one-size-fits-all in farming, there is likely no one-size-fits-all rallying cry that can capture all of the challenges, nor prescribe what to do next.

Perhaps a new slogan isn’t necessary. The low market prices say it all.

I would love to hear your idea of what the next agriculture rallying cry (or cries) should be in the comments!

Topsoil is handcrafted just for you by Ariel Patton. Complete sources can be found here. Thanks to Tina Marsh Dalton and Kevin Kohler for reviewing earlier drafts of this edition. All views expressed and any errors in this newsletter are my own.

If Topsoil has helped you understand the fascinating world of agriculture a little better, please like using the heart button below, subscribe, or share with an ag-curious friend!

I think the issue is more complex (as you've written about in past articles). These soybean and corn crops don't directly feed humans. Much of it goes to feeding livestock and for biofuel—a low-value use of the stuff because the EROI is just under 1.0. It's only economically feasible because of government subsidies. Rather than debating supply vs demand, we should scrutinize what that artificial demand is.

On a different note, there will always be humans who don't have enough food. We can argue that it's just a "distribution issue" or some other technological reason. But it comes down to ecological dynamics, or laws of nature. Modern man lives in a story that the world was made for humans, and that he can manipulate as much of nature to produce his food as he pleases. We take more and more land for industrial monocrops dependent on synthetic biocides and fertilizers. This increases the human population, which in turn requires more food (and energy, materials, land, water, etc.) in an endless feedback loop. Until we can change our view about our place in nature, we will always have BOTH apparent food overproduction and food scarcity. Understandably, many will not comprehend this argument without significant background information.

Excellent article! I've always thought that "feeding people" is more of a distribution issue than a production one.